My kid was turning 3 in a few days and we had planned a family get together. My parents had come over for the birthday and my in-laws were arriving that day.

Over lunch, the conversation meandered from my work to my dad’s post retirement life to my kid’s school admissions. (School admissions in Mumbai are no less difficult than cracking IITs/IIMs. The latter might be a tad easier.)

Amidst the talk, my father declared (my father normally doesn’t suggest, he declares) that he would gift my kid a FD (Fixed Deposit) to fund his education. While I suggested he should use his savings to go on a leisure world trip, he in his typical don’t-tell-me tone said “I have enough money for myself. My insurance policy is maturing next month and I shall gift that to my grandson.”

I curiously asked “which policy”?

He proudly stated “I started this policy when you were studying engineering. The policy provided life cover till maturity and a sum assured payable on maturity.”

“When you had a horizon of 18 years, why didn’t you invest in mutual funds?” I asked.

“Huh… Does your mutual fund give me insurance and the returns too?” he retorted.

“Wait.” I said.

I opened my laptop and quickly worked out some numbers in excel with the details my father gave me about the policy. In a few minutes, my answer was ready.

I said “Wouldn’t it have been better if you got 2.5 times the money that you are getting from your policy?”

He had been expecting an answer all the while, but this literally took him by surprise.

“WHAT THE HELL?” he exclaimed. “Are you kidding?”

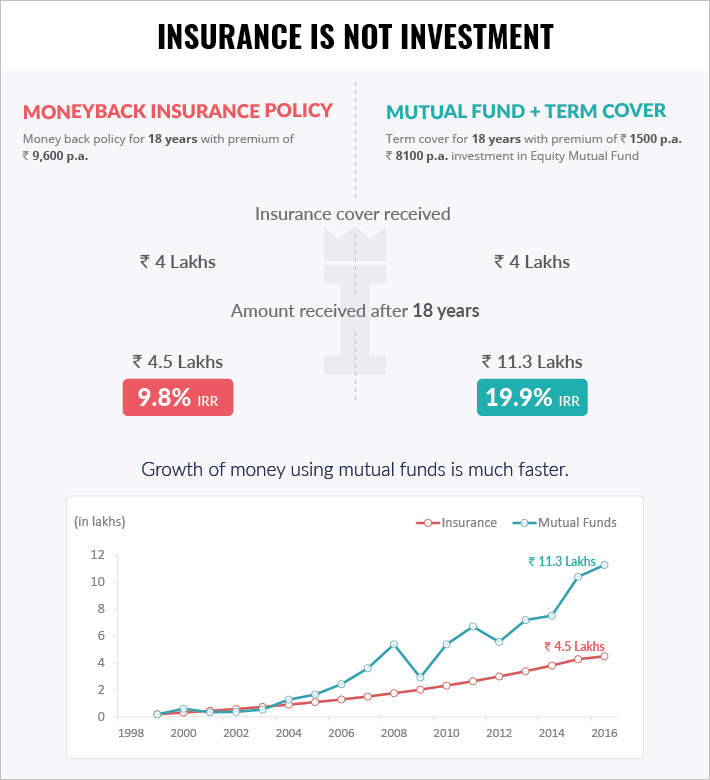

I explained him the concept as in illustration above (numbers used are sample but not misleading)

- Out of the 9600 that you invested every year, you got an insurance cover for 4 Lakh and sum assured on maturity equal to 4.5 Lakh

- The investments could have been alternatively done as following:

- Purchase a pure term cover of 4L for Rs. 1500 p.a.

- Invest remaining 8100 p.a. into mutual funds

Had he invested as in the second option, he would have been indifferent in terms of insurance, however, he would have had 2.5 times the money he would currently have.

Rather than 4.5L that the insurance policy is paying on maturity, investment in mutual funds would have given him 11.3L.

He murmured “Wow, that kind of thing would have even funded the Ivy league education for my grandson…”

The entrepreneur in me said “… or seed-funded his venture… who knows… “.

I noticed, my wife signaling something. It was time to pick-up my in-laws from the airport.

I pushed off to the airport, thinking – what gift is my father-in law getting?

Would it be deja-vu with another WT’X’ moment?

This article was originally published at Invezta