We all fall prey to bad habits in various facets of our life. Money is no different. Bad money habits developed from myths and perceptions could hold you back from being rich. Take a look at the habits and see if you have been guilty of any, or all 🙁 , of these:

1. I like to time the market

Investment returns are never equal to investor returns. Confused? Consider this: Dalbar Inc., a US based research company discovered that from 1985 to 2005 the S&P 500 averaged an annual return of 11.9% but the average investor during the same period made a paltry 3.7%. That’s because the poor investor tries to time the market. No wonder, at 21,000 sensex we all are aggressive and at 8,000 sensex we all are conservative. Rather than TIMING the market ‘TIME in the market´ is important.

2. I have 10 LIC policies. So, I’m insured

Most people believe this and that’s the reason why the average sum assured of a person buying insurance in India is a mere Rs.90,000. That’s because we mix investment with insurance. You should never INVEST in insurance, you should BUY insurance. By that I mean, Term Insurance (a pure risk insurance policy). But we never buy them. Why? Nobody sells them! What sells is junk insurance policies which gives the sales agent high commissions.

Got the following SMS from a pesky insurance agent the other day – The SMS reads: “PAY 15YRS GET DOUBLE OF UR PREMIUM FOR LIFE TIME Tax Free By LIC of India FOR DETAILS PLS CALL XYZ”. Sounds like an awesome deal? Complete bull. For those who like number crunching, a quick excel workout will reveal the returns at a measly 7.3%.

3. Gold and Real Estate. The perfect mix, na?

You buy gold as a fear asset or a hedge asset. Fear? Fear that something may go wrong & so gold will be the safe haven. Hedge? A hedge against inflation. Real Estate is an asset with too much sensationalism. I keep hearing stories like this: “My father bought this property in Bandra for just 5,00,000. We were lucky, yaar”. Whoever, thinks this is fantastic, please use an excel sheet to calculate the returns. You’ll be surprised. I am not against Gold and Real Estate as part of your portfolio. Have them, but do not consider them as growth assets. No. They’re not. They are saving assets. They will give you real return (post-inflation) of 1-2%. Of course there will be spikes in between but over longer periods (more than 10 years) they will never give equity kind of returns. Never.

4. Investments? I’m too young to start

This is the most common reason that we overhear when we ask someone about saving for their future. People feel their limited income will not spare anything to save. But believe me even a small amount kept aside every month can go a long way. So, even if the amount is petty what’s more important is that you are saving. If you need 50 Lacs after 20 years then you need to start saving Rs.5,500 per month from today. But wait for 10 years and the saving requirement grows to Rs.22,500. Need we say more?

5 Tax Planning = Financial Planning

“Saar, this is the last week for making this investment” says the insurance agent (more on this later). It works amazingly well especially if your HR is behind you to give the 80C documents else your tax will be deducted.

Result? You end up buying a junk product without really getting the big picture. Apparently, for a majority of us, Tax Planning (forced saving) = Financial Planning.

6.FD’s, PPF, NSC are the best and safest

No doubt all these are safe but they are best in terms of savings and not investment. Remember, Savings is linear; investing increases your wealth. That’s because the post-tax return that you earn on these products will hardly beat inflation. As Warren Buffet puts it in his latest letter to shareholders “Bonds promoted as offering risk-free returns are now priced to deliver return-free risk.”

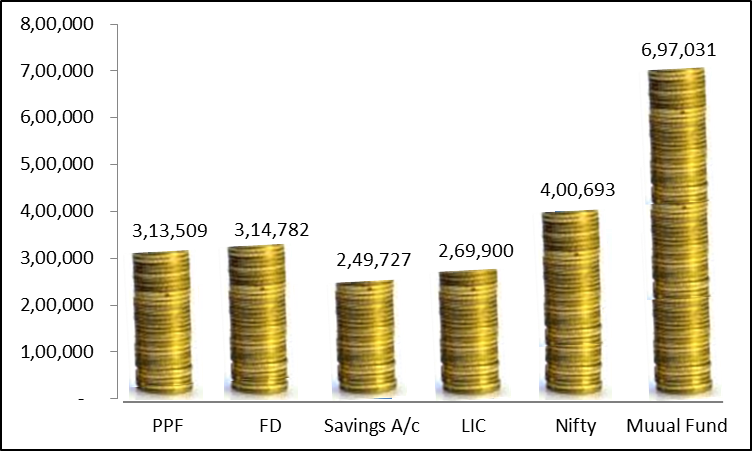

The accompanied chart shows the amount you would end up accumulating after investing Rs.20,000 per annum in various investment products for 10 years starting 2002

Let’s decode this: Assuming average inflation was 7% in this period (in reality it was much higher) your savings should have grown to Rs.2,95,000 to just beat inflation. Just check yourself if you have actually become richer or poorer.

7. I am too young to plan for retirement

If you feel you are too young to think about retirement you are wrong. One good thing about you being young is that compound interest and time is on your side. The earlier you start the better it is to benefit from the power of compounding. More than the stock or mutual fund, the age at which you start investing determines how much wealth you build.

BONUS. You know you are wasting your time (& money) if you hear this from a sales agent:

- “You just have to pay for 5 years and you get free cover for life”

- “This policy comes with free insurance”

- “This is the last week for making this investment”

- “This is a new fund. The NAV is only Rs.10. Saar, you will get more units, saar”

- “The returns are guaranteed, saar”

- “The Fund is going to declare a dividend of 200%, so buy it as soon as possible”

If you have been on the receiving end of all this $*&*^$# you are not alone. Rich, Poor, Educated, Illiterate, Men, Women, Doctors, Engineers etc. have been all duped in the past at least once. After all mis-selling is only half the story. The bitter pill, the other half, the un-said story is MIS-BUYING!

At Futurewise, we help people come out of this mess and organize their finances in a whole new way. Financial Planning is generally a fee based service but we at Futurewise are offering the same services for FREE to our early adopters.

You can sign up here for Free: Sign up Page.

Do watch this 2-minute video to better understand our services: Watch Video

Download a sample financial plan we prepare for our clients: Sample Financial Plan

Ronak Hindocha is the Founder of Futurewise Financial Planners; a company that helps people manage and organize their finances in a whole new way. He can be reached at +91-22-29652244 or ronak.hindocha@futurewise.co.in.

Ronak

@Kiran. Sorry Kiran. We are looking into the issue. We will email you as soon as the registration page is live again.